When you take out a mortgage, whether it be to purchase or refinance a home, you must pay closing costs. These costs can vary and it’s important to know which costs are negotiable.

There are fees that must be paid to the lender, those that must be paid to third parties (such as title/escrow and insurance), and finally those that are optional, such as mortgage discount points.

Whether you pay these fees out-of-pocket is optional, but the costs are not and you must pay them in one way or another.

Two Types of Closing Costs

There are two main types of closing costs, there are “recurring closing costs” and “non-recurring closing costs”.

Non-recurring closing costs are those which are charged just once and at, or prior to closing. Recurring costs are those that will be charged more than once.

Here are some examples of non-recurring closing costs (one-time fees):

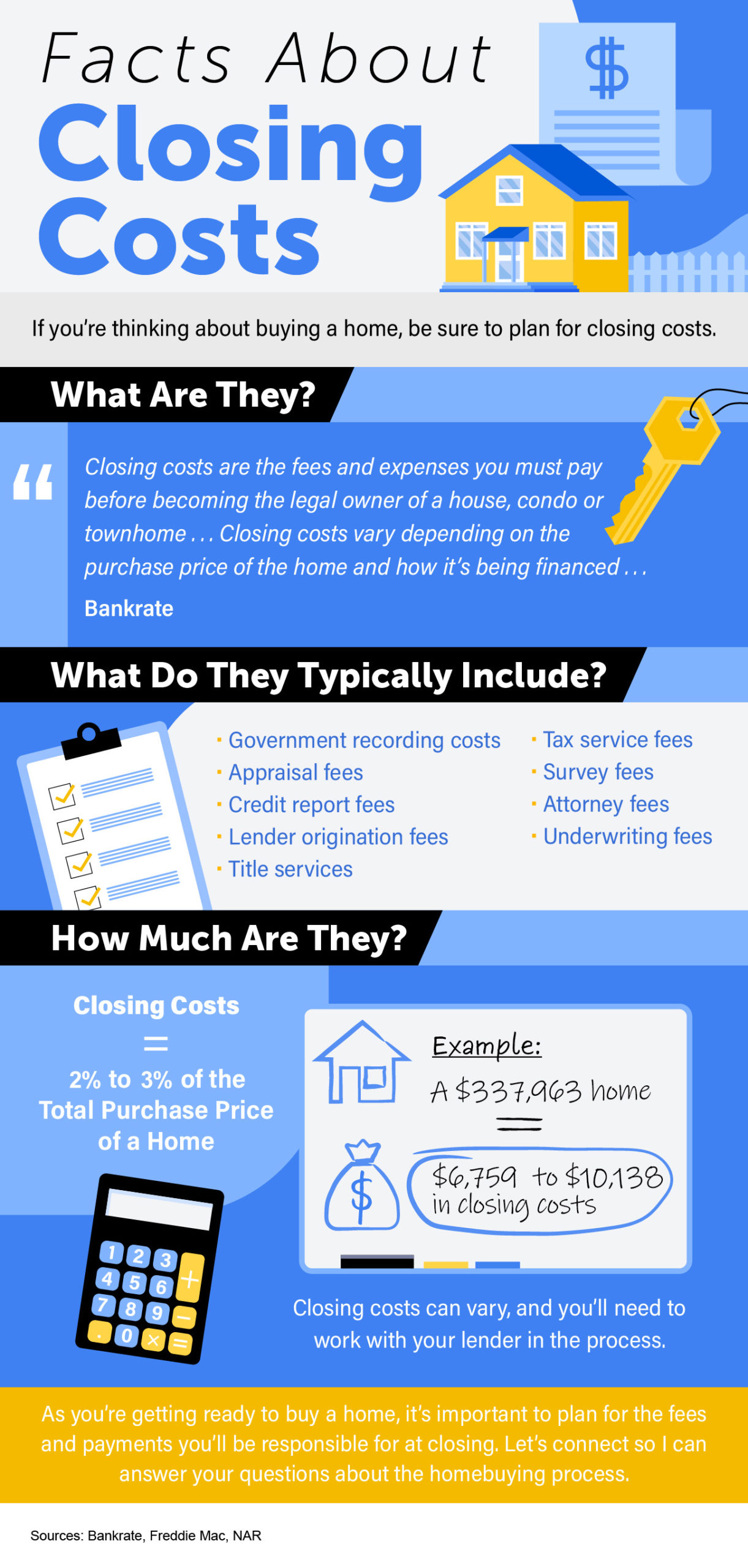

– Lender fees (underwriting, processing)

– Loan origination fee

– Mortgage discount points

– Credit report fee

– Appraisal fee

– Home inspection fee

– Title and escrow fees

– Doc prep fees

– Recording and wire fees

– Notary and messenger fees

– Transfer taxes

Here are some examples of recurring closing costs (paid more than once):

– Homeowner’s insurance

– Mortgage insurance

– Property taxes

– Interest

– HOA dues

*Not all fees are applicable depending on the property, location, loan type, etc.

As you can see, there are a number of costs associated with obtaining a mortgage and these costs tend to average approximately 2-3%. The average home value in Central Ohio currently stands at $337,963 and thus closing costs could be between $6,759 and $10,138.

Not everyone has the cash on hand to pay for all these fees in addition to the required down payment, while others simply prefer to keep more cash on hand. But you do have options when it comes to closing costs and whether you pay these fees out-of-pocket is largely up to you.

If you want to reduce your closing costs, there are a few strategies to do so.

Use Seller Contributions to Cover Closing Costs

If yours is a purchase transaction, one of the most common ways to reduce your out-of-pocket closing costs is to request a contribution from the seller.

These “seller contributions” can be used toward the closing costs mentioned above, but cannot be used for the down payment, nor can these funds wind up in the buyer’s pocket (and thus they must be applied in full to the allowable closing costs).

When negotiating a sales price, the buyer and seller can discuss contributions. Their inclusion will likely lead to a higher contract price as if a home is listed at $200,000, and the buyer offers $195,000 with a request for 3% towards closing costs ($195,000 x .03 = $5,850) the seller will see this as an offer for $189,150 (value after the seller pays the $5,850 towards your closing costs).

As a result, the buyer still pays the closing costs by accepting a higher loan amount associated with a higher purchase price. However, the costs aren’t paid at settlement, so it’s easier for the buyer short on cash.

The maximum amount of seller contributions allowed will vary based on the type of loan (conventional vs. FHA), the property type, and the LTV ratio. The lowest amount allowed is 0% of the purchase price, and the highest allowed is 6% (an average is closer to 2-3%).

Just be careful when combining credits to ensure they don’t exceed the maximum allowed by the lender. Assuming you find that you’re leaving money on the table, consider using the excess to buy down your rate.

Get a Lender Credit to Offset Closing Costs

Another way to reduce or eliminate your out-of-pocket closing costs is via a lender credit. Essentially this is your agreement to take a higher mortgage rate in exchange for lower settlement costs. The higher rates offsets the expense of the closing costs. This works on both purchases and refinances.

For example, a lender might tell you that you can secure an interest rate of 4.25% paying $5,000 in closing costs, or give you the option of taking a slightly higher rate, say 4.5%, with a $3,500 credit back to you.

If all your costs are paid via a higher rate, it’s a no cost loan, though sometimes this definition only covers lender fees, not third party fees.

Either way, you’ll pay a bit more each month when making your mortgage payment, but you won’t need to come up with all the money for the required closing costs.

Again, your out-of-pocket costs are reduced here, but you pay more throughout the life of the loan via that higher mortgage rate. That’s the tradeoff.

Negotiate and Shop Your Closing Costs

It’s also possible to shop around for certain settlement costs. For example, you can comparison shop for lenders, home inspectors and/or your homeowner’s insurance and save on costs there. The same goes for your home inspection.

If refinancing your mortgage, ask for the “reissue rate” or “substitution rate” when purchasing the lender’s title insurance policy. There is no reason you should have to pay full price again for a title search when you’ve been the only person living in the property. This could save you as much as 30% on the cost of your title insurance policy and thus a significant amount of money on closing costs with a simple phone call to the title company.

Similarly, when looking for a bank to work with, be sure to look closely at the fees they charge. They don’t all charge the same fees or the same amounts, so finding a lender with a low rate and low fees could save you big. Lenders are required to provide applicants what’s known as a Good Faith Estimate (GFE), these documents include the estimated costs you’ll pay for a loan with them including the Annual Percentage Rate (APR), a number that is used when comparing mortgage loan offers.

Also watch out for unnecessary junk fees, which can really add up. But remember that certain closing costs just aren’t negotiable, like property taxes.

What Else?

There are a few other ways to cut down on closing costs. Prepaid interest, which is the per diem interest due between the time you close and your first mortgage payment, can be costly depending on the size of your loan and when you close.

If you close near the end of the month, you can greatly reduce the number of days of per diem interest due at closing. This can significantly reduce your closing costs.

For those refinancing, it may also be possible to roll closing costs into the new loan, instead of paying them out-of-pocket.

Again, the downside here is that you’ll be paying interest on those closing costs for as long as you hold your mortgage, as opposed to just paying them at face value upfront.

But it’s worth consideration, especially if you don’t plan to stay in your home, or with the mortgage very long.

One Final Tip

While closing costs can be expensive, one of the largest mortgage expenses is the interest rate. Over the life of the loan, a few small percentage points can result in hundreds of thousands of dollars in interest payments.

One of the best ways to lower your interest rate? Shop around and compare lenders!

Related Article

10 Things You Should NOT Do While Buying a Home

10 Questions to Ask the Lender When Applying for a Mortgage

Understanding Mortgage Rate Locks

If you, or someone you know is considering Buying or Selling a Home in Columbus, Ohio please give us a call and we’d be happy to assist you every step of the way!

The Opland Group Specializes in Real Estate Sales, Luxury Home Sales, Short Sales in; Bexley 43209 Columbus 43201 43206 43214 43215 Delaware 43015 Downtown Dublin 43016 43017 Gahanna 43219 43230 Grandview Heights 43212 Galena 43021 Hilliard 43026 Lewis Center 43035 New Albany 43054 Pickeringto, 43147 Polaris Powell 43065 Upper Arlington 43220 43221 Westerville 43081 43082 Worthington 43235

Connect with us