Almost every major US housing market is plagued by short supply. In fact, inventory nationally for pre-owned properties is at 3.9 months, down 10.4% from last year, this according to the National Association of REALTORS® (NAR) in a recent report.

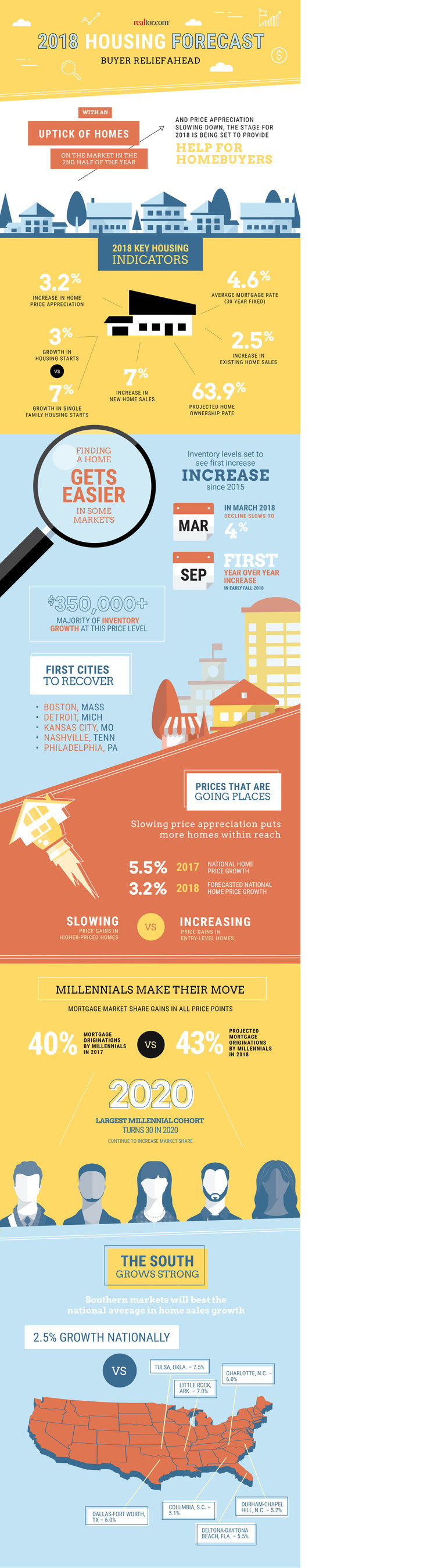

The challenge, according to Realtor.com®, could moderate in the next year. Groundbreaking is projected to ramp up 3%, with single-family starts up 7%, as revealed by Realtor.com’s 2018 National Housing Forecast.

The catch? Activity won’t kick up until later in the year, and most new homes will be the mid to high ends of the market (not the starter / first-time buyer level)—not an ideal scenario in the short term. Lower-priced entry level homes, (which were hit hardest in the recession, as banks simply weren’t lending to buyers at this level of the market unless they had exceptional credit) are especially scarce—down 20.4% year-over-year over the summer.

. As credit requirements have loosen buyer demand rose significantly exceeding supply. Unfortunately the cost of land, construction materials, land and permits also rose during this time which has prompted most of the builders to focus their construction efforts on the middle and upper ends of the market, price points in which builders can earn a healthier profit as buyers in these price points typically more inclined to spend money on the builder’s upgrades.

“We are forecasting next year to set the stage for a significant inflection point in the housing shortage,” says Javier Vivas, director of Economic Research for Realtor.com. “Inventory increases will be felt in higher-priced segments after home-buying season [in the fall], which limits their impact on total sales of the year.”

Home prices will increase in 2018, but at a weaker pace than in 2017, the forecast shows: 3.2%. Home prices in the starter end of the market are likely to buck this trend and will continue to be driven but short supply and a lack of desirable inventory. Existing-home sales are expected to grow 2.5% to 5.60 million. Considerable gains in prices and sales will be seen in: Las Vegas-Henderson-Paradise, Nev.; Dallas-Ft. Worth-Arlington, Texas; Deltona-Daytona Beach-Ormond Beach, Fla.; Stockton-Lodi, Calif.; Lakeland-Winter Haven, Calif.; Salt Lake City, Utah; Charlotte-Concord-Gastonia, N.C.; Colorado Springs, Colo.; Nashville-Davidson-Murfreesboro-Franklin, Tenn.; and Tulsa, Okla.

Columbus, OH Ranked as one of the country’s Top 10 Housing Markets for much of 2016-2017 and this trend is likely to continue as our local economy and job growth remains strong.

Realtor.com also anticipates 43% of buyers in 2018 will be millennials, up from the 40% projected for 2017. The biggest group of millennials is turning 30 in 2020, so their share is likely to continue tracking upward.

Expected to grow, as well, are mortgage rates, averaging 4.6% and possibly reaching 5% by year-end, the forecast states. Action by the Federal Reserve and economic factors, including inflation, will precede the rise. Markedly, more first-time homebuyers were able to get a Federal Housing Administration (FHA) mortgage this year than last year, despite a rate uptick. The 30-year, fixed mortgage rate averages 3.92% at present, according to Freddie Mac.

Higher mortgage rates will eat into buyers’ budgets, putting even more price pressure on the most affordable homes for sale. Unless there is a fundamental shift in the number and type of homes for sale, this appears to be the new normal of the American housing market.

One factor in the health of the housing market is the homeownership rate; experts predict it, too, will rise, though slightly, to 64 percent. The homeownership rate has improved twice thus far this year, up to 63.9 percent in third quarter, according to the Census.

A potential wrench is tax reform. The forecast was made prior to the House bill passing and the Senate bill being voted on; as such, Realtor.com cautions that certain cuts—among others, the mortgage interest deduction and the state and local tax (SALT) deduction—could lead to less in the way of prices and sales.

The forecast, however, is optimistic overall.

“As we head into 2019 and beyond, we expect to see these inventory increases take hold and provide relief for first-time homebuyers and drive sales growth,” Vivas says.

If you, or someone you know is considering Buying or Selling a Home in Columbus, Ohio please contact The Opland Group. We offer professional real estate advice and look forward to helping you achieve your real estate goals!

The Opland Group Specializes in Real Estate Sales, Luxury Home Sales, Short Sales in; Bexley 43209 Columbus 43201 43206 43214 43215 Delaware 43015 Dublin 43016 43017 Gahanna 43219 43230 Grandview Heights 43212 Hilliard 43026 Lewis Center 43035 Marysville 43040 43041 New Albany 43054 Pickerington 43147 Powell 43065 Upper Arlington 43220 43221 Westerville 43081 43082 Worthington 43235

Connect with us