Click on the image to enlarge

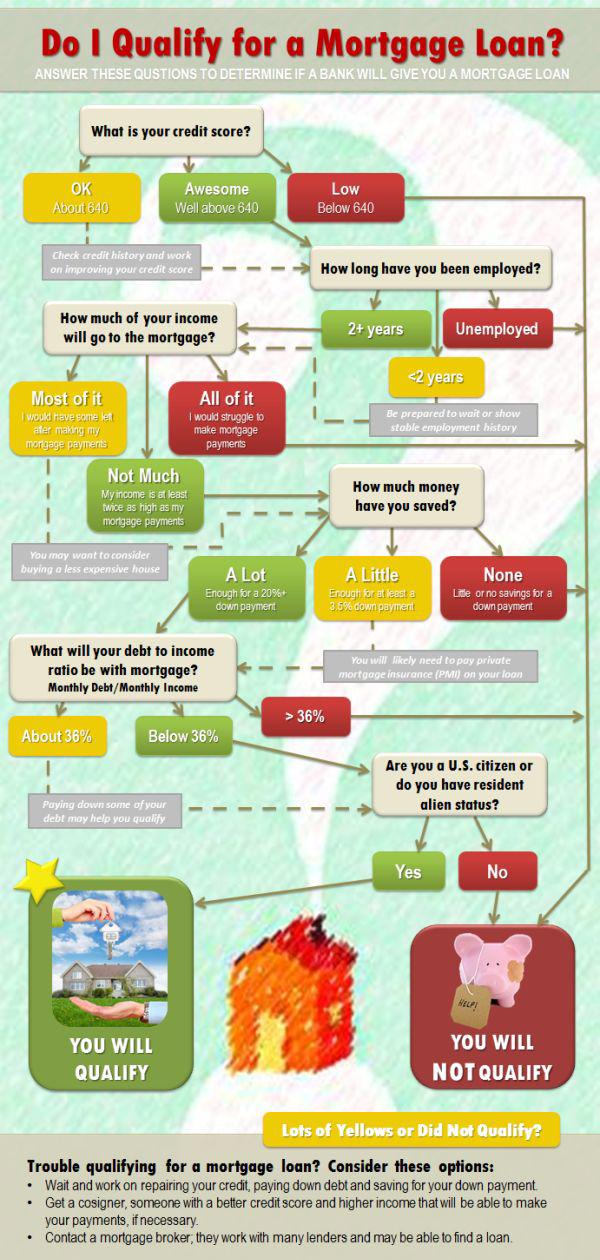

Qualifying for a mortgage can be very simple. There are minimum requirements such as credit scores and debt to income ratio. If you meet these requirements, you will be approved for a mortgage.

The two main factors the lender will take into consideration are your credit score and your debt to income ratio. These factors will let you know your spending power, or how much the lender is willing to let you borrow.

The lender will allow you to borrow the money for different lengths of time, this will directly affect your monthly payment. For example: if you do a five-year mortgage, it will be a hefty monthly payment compared to a 30 year mortgage. A 30 year mortgage will greatly reduce your monthly payment, but in the long run you will pay more interest.

Also be careful if you do get approved. DO NOT go buy other items like a car or furniture. This will affect your ability for the bank to be Committed for a loan. You will go through the whole process and in the end, you will not be able to close on the purchase of your home.

Minimum Requirements – Most lenders have minimum requirements in order to approve you for a loan. These requirements will vary from lender to lender. For instance, a bank will have a minimum credit score that could be different from a credit union, or a mortgage broker and vice versa. The lender will also require a debt to income ratio that satisfies the ability to repay the loan.

Credit Score – When comparing your credit score to the lenders requirements the lender will then provide you with options. Examples of the options are, Government loans and Conventional loans.

The Government loan will accept a lower credit score, this type of loan is called an FHA. If your score is high enough to be accepted by the primary market, and you might will be offered a Conventional loan. There are “pros and cons” to each type of loan.

The current norm is a minimum credit score of 620-625 for a FHA Loan and a 640 for a Conventional loan. We are currently working with lenders that are approving buyers with the credit score as low as 580. This lower credit score will require certain circumstances that allow the lender to forgive a current low credit score.

Also be careful of shopping your rate. Each lender will check your credit score. Checking your score will affect your credit negatively if done too many times. If you already know your score tell the lender not to run your credit. See What is a Good Credit Score and What Do You Need to Buy a Home

Debt vs Income Ratio – The debt vs income ratio has minimum requirement in order for you to qualify for a loan. The debt vs income ratio is determined by to factors. The overall annual debt vs income and the monthly expense debt vs income. The lender will want to see that your spending is low enough to pay back the loan.

When looking for the debt, the lender is looking for your current liabilities. Examples are car payment, credit cards, student loans, child support and any revolving account you are making payments on. Other everyday expenses will not be included like gas, groceries, entertainment ect.

Term – Term is another way to say period of time. First-time homebuyers will usually go with the 30 year term. The 30 year term will have a reduced monthly payment. The homeowner that is upgrading will usually go with a 15 year term. The 15 year term will have higher monthly payments, but the property will be paid off much quicker at a lower interest rate.

The difference between the two payments, is usually about 35%-40%. So for example if a 30 year mortgage has a payment of $1000 a month. The 15 year term will be $1,300-$1,400.

There are other options as far as term you can do a 5 year, 15 year, 20 year and 30 year. It all depends on your lender that you choose. Also always ask your lender is this all my options?

If you, or someone you know is considering Buying or Selling a Home in Columbus, Ohio please give us a call and we’d be happy to assist you!

The Opland Group Specializes in Real Estate Sales, Luxury Home Sales, Short Sales in; Bexley 43209 Columbus 43201 43206 43214 43215 Delaware 43015 Downtown Dublin 43016 43017 Gahanna 43219 43230 Grandview Heights 43212 Galena 43021 Hilliard 43026 Lewis Center 43035 New Albany 43054 Pickerington 43147 Polaris Powell 43065 Upper Arlington 43220 43221 Westerville 43081 43082 Worthington 43235

Connect with us

-

1. What fees will I have to pay?

Closing costs, prepaid fees (i.e. taxes and insurance) and title fees are all associated with most loan transactions. A good faith estimate is provided to you once you have executed a loan application, which lists all of your specific fees. A sample mortgage analysis can be provided in advance of a full application upon request. At this time, Walden Mortgage does not require an application fee at the time of application.Although most loans require an escrow account for the pre-payment of taxes and insurance, some borrowers will have the option, on some loans, to bypass the need for an escrow account, thus lowering the prepaid fees at closing. 20% or more down payment is required to remove the escrow requirement and some fees may be associated with the election to bypass the escrow account. -

2. Do I have to put any money down when purchasing a home?

Depending on the type of loan program, some programs offer 100% financing or down payment assistance. For most conventional loans, a 5% down payment is required and for FHA loans, a down payment of 3.5% is required except for those cases where down payment assistance is obtained. -

3. How long will my refinance take? How soon can I close?

A refinance takes approximately 2-4 weeks from the time you sign your loan application to the time you close. Once we have received your application and any additional documentation (i.e. bank statements, pay check stubs, appraisal, etc.), your loan is submitted for approval. Once the approval is received, your loan documents will be drawn and sent to the title company for your signature. If you are refinancing your primary residence, keep in mind a three day right of rescission is required before your loan can fund. In some cases, an appraisal may not be required and the loan can close more quickly. -

4. What are the basic types of mortgages?

Conventional (Fannie Mae and Freddie Mac insured mortgages), FHA (Federal Housing Administration, under the U.S. Department of Housing and Urban Development), VA (U.S. Department of Veterans Affairs), RHS (U.S. Department of Agriculture) and certain non-conforming loans including JUMBO loans whose loan amounts exceed that approved by Fannie Mae and Freddie Mac for conventional loans. -

5. What is the difference between a mortgage banker and a mortgage broker?

Mortgage bankers originate, and “fund”, their own mortgage loans. This means that they put up the money and handle the closing for the loan (regardless of their intent to sell or retain the mortgage servicing of the loan). A mortgage broker acts as a middle man who can shop several different mortgage banks to find the best deal to suit their customer. Typically a mortgage bank only offers one set of loan programs and rates whereas a mortgage broker can shop the loan to the bank with the best program and rate among several.Walden Mortgage Group is a mortgage broker whose funding source is that of a corresponding lender. This means we have a direct lending relationship with one bank, which in turn has access to several other large lending institutions. This close relationship with the funding source enables us to work directly with the source of the money to ensure prompt closings as our broker relationship allows us to be flexible in our product lines and pricing. We truly have the best of both worlds! -

6. What documents do I have to provide?

It depends upon the loan program you seek, the quality of your credit and the size of your down payment. On a typical fully documented loan application (where an applicant is seeking to qualify based on an employee salary), the lender will require: one or two current pay check stubs, W-2’s for the prior one or two years and bank and investment accounts statements for the previous one or two months, Federal Tax Returns, drivers license and a phone number for the insurance agent on the property in question. If an applicant is self-employed (has 25% or greater ownership in a business) then additional documentation may be required (i.e. 1040’s, 1165’s & 1120’s). -

7. How much loan can I qualify for?

The amount of a loan for which you qualify is based on two different calculations. Using what are know as qualification ratios, lenders evaluate your income and long term debts to determine a “safe” amount for your mortgage payments. A fairly standard ratio is 33/38. This means 33% of your gross monthly income (GMI) for your “front end” ratio which includes only your house payment and 38% of your GMI for your “back end” ratio which includes your house payment and all other obligations (i.e. auto payments, student loans and credit cards). Certain mortgage plans sometimes allow for more liberal ratios (FHA allows for up to 55% back end ratio although not every lender will provide a loan at ratios that extreme). -

8. What are points?

In the special vocabulary of mortgage lending, “points” are a type of fee that lenders charge (the full-term to describe this fee is “discount Points”). Simply put, a point is a unit of measure that means 1% of the loan amount. So, if you take out a $100,000 loan, one point equals $1,000. Discount points represent additional money you can pay at closing to the lender to get a lower interest rate on your loan. Usually, for each point on a 30-year loan, your interest rate is reduced by about .25% of a percentage point for 1 discount point (1% of the loan amount). TIP: Usually, the longer you plan to stay in your home, the more sense it makes to pay discount points. We will be happy to discuss the pros and cons with you to help you make your decision. -

9. What is a loan origination fee?

Income derived as a fee charged to the borrower by their lender for making a mortgage loan. This fee is usually computed as a percentage of your loan amount (1% origination fee = 1% of the loan amount). As a standard practice, Walden Mortgage Group does not charge a loan origination fee as a percentage of the loan as our income typically comes from our lending relationship; however we use that section of the Good Faith Estimate to lump our miscellaneous fees for processing the loan application. This fee, like most, is due and payable at closing. -

10. What is PMI (private mortgage insurance)?

If you put less than 20% down on most loans, you’ll be asked to protect the lender by carrying private mortgage insurance (PMI). Carrying PMI ensures that the debt is repaid if you default on the loan. This charge adds approximately an extra half a percent onto the loan. If you have reached 20%, you can contact the lender to see about dropping PMI. In most cases, the lender will not consider dropping PMI until you have owned your home for 2 years. However, once you have reached 22% equity, the lender is required by law to drop PMI. Ask one of our experts how you can avoid paying PMI. -

11. What is mortgage interest? What is a 1098 form?

Mortgage interest is calculated based on your interest rate on an annual basis. You will receive a 1098 mortgage interest statement in January each year, which totals the amount of interest you have paid on your loan for that year. Lenders are only required to report mortgage interest if you have paid $600 or more in interest. This means that in most cases, you will not receive a 1098 if you have paid less than $600. -

12. What is the difference between locking and floating an interest rate?

Locking a rate means that you have agreed on an interest rate with your loan officer, at which time he/she will make a formal agreement with the broker or correspondent that your loan will be serviced by. Floating an interest rate is used when the market is volatile and your loan officer believes that the rates could improve. Basically, your loan will be registered in the system, but your rate has not been locked. -

13. What is the difference between conforming and non-conforming loan amounts?

The term “conforming,” as opposed to “non-conforming,” is used to classify loans that fall within the guidelines as set forth by Fannie Mae and Freddie Mac. These are the two private, congressionally chartered companies that buy mortgage loans from lenders, thereby ensuring that mortgage funds are available at all times in all locations around the country. These loans generally offer the most attractive rates. Conforming loan amounts are $417,000 and below. Non-conforming loan amounts are above $417,000. These loans are usually called a “JUMBO” loan. -

14. What are FICOs?

FICO stands for Fair, Isaac Corporation, which developed the formula for credit scoring. The term also applies to the credit score itself. A FICO score can range from 300 to 850. In general, the higher the score, the more credit-worthy a borrower is in the eyes of the lender. A score of at least 680 indicates the borrower is very creditworthy. -

15. Should I choose a fixed or an adjustable rate mortgage?

You can choose a mortgage with an interest rate that is fixed for the entire term of the loan or one that changes throughout. A fixed-rate loan gives you the security of knowing that your interest rate will never change during the term of the loan. An adjustable-rate mortgage (called an ARM) has an interest rate that will vary during the life of the loan, with the possibility of both increases and decreases to the interest rate and consequently to your mortgage payments. Adjustable rates typically start lower than fixed rates but depending on the market at the time of “Adjustment” could wind up higher than a fixed rate. So the question of whether to go with a fixed or an adjustable is a personal decision that you have to make based on your tolerance for risk. -

16. What is APR (annual percentage rate)?

This is an interest rate index reflecting the cost of a mortgage as a yearly rate. It is not the rate your payments are based on but a combination of the interest rate, points and other lender fees. Because of this, the APR is almost always higher than your interest rate.The APR is supposed to allow homebuyers to compare different types of mortgages based on the annual cost for each loan. However, because not all lenders include all their fees in the APR calculation like they are supposed to, the comparison of APR’s is almost useless. It is far easier and more accurate to request a “Good Faith Estimate” from all lenders when you are shopping for a loan. A Good Faith Estimate will show all points, lender fees and the interest rate. Simply add up all the lender fees and count the total cost in dollars, not the APR. -

17. Can I use a gift for a down payment?

Yes. Certain loans allow a relative or close friend to provide 100% of the down payment as a gift, but the lender will ask that a “Gift” letter be signed by the donor stating that the gift funds are not expected to be repaid. The donor will also have to show a bank statement or other paperwork proving the gift came from their account. Some loan products require a 20% down payment if the source of the down payment is exclusively from gift funds. -

18. Can I borrow funds for a down payment?

Yes. It is possible to borrow against an asset that you currently own for the down payment. For example you can borrow against your 401(K), assuming that your company plan permits it, and you could also borrow against your current residence to purchase a new one (i.e. a bridge loan or an equity line). You may also borrow against your fully invested stock portfolio, avoiding the tax consequences of selling prematurely. Some loan programs allow you to borrower unsecured personal loans to help with the costs. -

19. What is homeowner’s/hazard insurance?

Homeowner’s insurance protects both the owner as well as the lender against the occurrence of physical damage to the property (i.e. fire or burglary). Some perils are not generally covered by the standard homeowner’s polices, for example floods and earthquakes. -

20. What is flood insurance?

If your property is located in a flood zone, you may be required to obtain flood insurance. The appraiser will research the area and determine if the property is in a flood zone. Also, A flood certification is executed at closing, which will determine whether you will need flood insurance. -

21. What is lenders title insurance and why do I need it?

Before you purchase a property or close on a new loan, it’s essential to know that the title to the property will be free and clear, free of prior defects and indebtedness. A homeowner and prospective lender need to be certain that what is available on the property is what is referred to as a “marketable title”. A title company researches the legal history of the property, which entails searching public records in the offices of the county recorder. Problems with the title could threaten the mortgage, limit ones use and enjoyment of the property and could result in financial loss. A policy of title insurance protects a homeowner’s title and the insurer covers the cost of any legal challenges. All lenders require a title insurance policy before they will fund your loan. Lenders Title Insurance is required on all first mortgage loans in the state of Kentucky and insures the lenders interest in the marketable title. Owner’s Title Insurance is available upon request to protect the buyers interest in marketable title. -

22. What is a loan prepayment penalty?

A prepayment penalty on a loan allows the lender to charge a borrower additional interest, typically six months worth, when a loan is repaid during the penalty period, which is usually somewhere in the first three to five years of the loan. If a loan does have a prepayment penalty, this is clearly stated within the mortgage disclosures, mortgage note or prepayment penalty rider to the note. The advantage of taking a loan with a prepayment penalty is that it could carry a lower rate of interest or you may be permitted to take a loan without paying for non-recurring closing costs. -

23. Will I receive a copy of my appraisal once I close?

Yes, typically provides you with a copy of your appraisal before or at the closing of your mortgage transaction.